A K-shaped world

Two major market themes are pulling the world economy in two different directions at present. On the one hand, the onset of war in the Middle East has made a spike in inflation rates across all economies inevitable in H2 2026 and into 2027: this has profound implications for the (likely upward) direction of interest rates and bond yields and further erodes the ability of consumers to continue to drive GDP growth. On the other hand, the perceived productivity benefits of a boom in spending on AI has propelled the valuation of Tech stocks worldwide to extreme levels, taking major stock markets to fresh all-time highs. This dichotomy, a “K-shaped outcome” has widened so far in Q2 2026.

When market and economic signals are so divergent, portfolio construction should hedge the uncertainty via, largely, balanced positioning. Our proprietary EnCor asset allocation model trimmed weights in equities, chiefly in the out-performing Czech market, at the end of April, raising cash levels and sought to reduce currency risk through holding more CZK-denominated bonds. Positions in commodities were retained at Q1’s levels, providing some protection against the coming inflation spike.

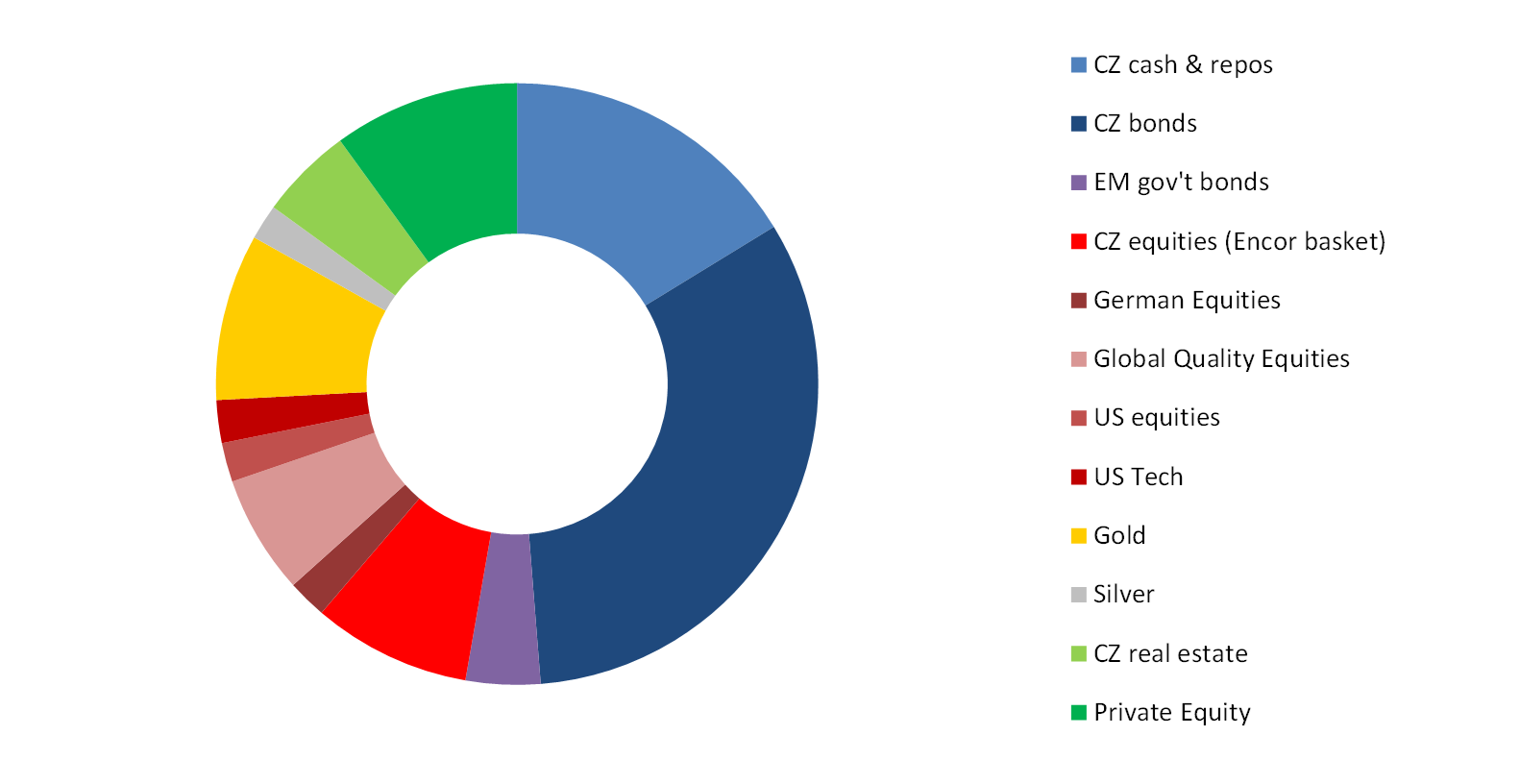

Allocation for a typical moderate risk client into Q2 2026*

Source: EnCor Wealth Management proprietary asset allocation model.

See disclosures at the bottom of this text. * Weights as of end April.

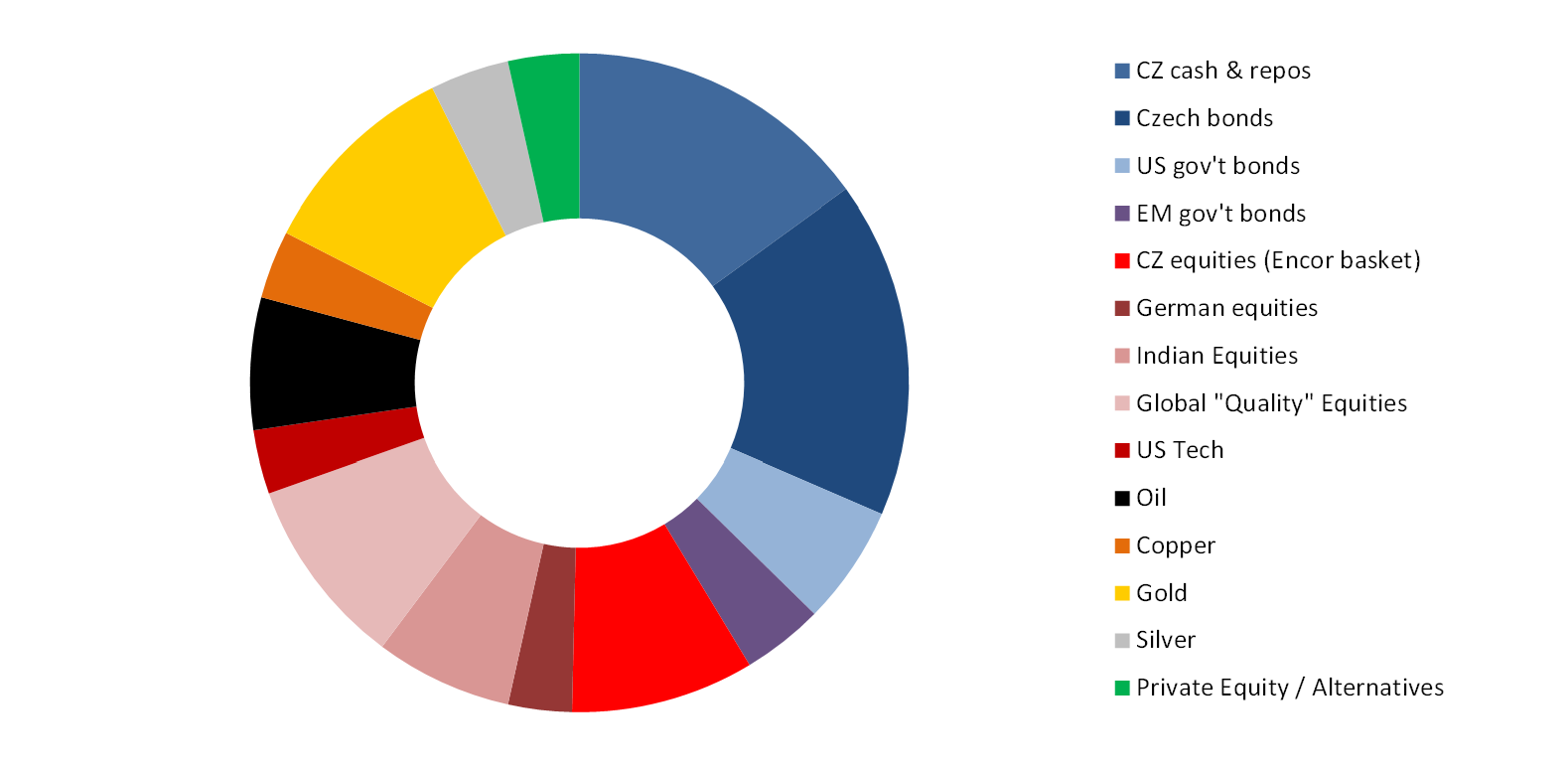

Allocation of our “Rustovy” Dynamic OPF – Q2 2026*

Source: EnCor Wealth Management proprietary asset allocation model.

See disclosures at the bottom of this text. * Weights as of end April.

March’s onset of the US-Israel-Iran war changed the outlook for interest rates and bond yields in the world economy, certainly looking out over 12-18 months. The March-May hikes in commodity prices, caused by supply disruptions, will, with certainty, feed through into energy, food and basic industrial input inflation rates over the coming months and quarters. While the Iran War may have halted, supply chains are not back to normal. Financial markets have had to price in potential interest rate rises and, by and large, had done so by the end of March. Higher inflation and higher borrowing costs will further erode the purchasing power of consumers across major and emerging market economies. Lower future demand for goods and services does really matter, as consumption makes up, for example, c.70% of US GDP at present. Demand in Western economies had only just recovered from the last inflation shock (2022-24) and these end consumers face also the possibility of increasing unemployment resulting from widespread AI adoption in corporate and government arenas.

There is no doubt that AI will boost productivity in the world economy going forward. Weights in a US Tech sector ETF give us exposure to this phenomenon. Valuations of companies involved in the delivery of AI, ranging from the model developers, the chipmakers, data centre providers and even energy providers have expanded, some in the Tech space to levels beyond those seen in the “Dotcom bubble” of 1999-2000. Whether the present AI mania in equities carries on, subsides or evaporates as a driver of valuations depends on the amount of capital expenditure, the achievement of returns, competition factors and feasibility of the business models. What is the case is that equity volatility rises when valuations expand, when IPOs come to market at very high multiples and thus the summer months could well be a bumpy ride for investors.

Commodities were among the strongest performers among asset classes in 2025 and into 2026. Our higher-risk portfolios hold positions in all four of the key investment commodities, namely gold, silver, oil and copper. This balanced approach meant that our higher-risk portfolios were protected to a degree by holding oil as it spiked due to the onset of war in March. Since mid-May, commodities have peaked as an asset class, with most selling off but the global CRB Commodities Index is still up well over 20% on a year-on-year basis. The second-round inflation effects of the Iran War shock will course through the world economy in H2 2026-into 2027, as will higher microchip prices for consumer goods. The 1970s proved that commodities were the best hedge against higher and volatile inflation and they remain a building block in our portfolios for the present.

Our asset allocation for Q2, with weights spread among equities, commodities, and mainly Czech bonds is positioned for volatile markets, as investors absorb constrasting news-flows from a global “k-shaped” economy. Our larger cash positions look to dampen volatility for our clients’ portfolios until the path of the global economic growth, consumption and inflation becomes clearer.

Disclaimer: This article does not constitute an investment advice, or a recommendation to buy or sell a specific security. Please contact us at welcome@encorwealth.com if you would like to consult on your individual situation.

Author: Mark Robinson (11 June 2026)